What is financial independence (FI)?

It is typically defined as having enough income (from investments, passive businesses, real estate, etc) to pay for your reasonable living expenses for the rest of your life. You have the freedom to do what you want with your time (within reason). Working (full or part time), hobbies which generate income, or other activities are optional at this point.

- Reducing expenses – Reducing your living expenses to a reasonable level is the most critical step. Five-star restaurants, vacation homes, and jets are generally not achievable as a reasonable financial independence goal. But if you can realize contentment with significantly lower expenses, your ability to reach financial independence is greatly improved.

- Increasing income – Forget get rich quick schemes. There are plenty of those underemployed who should look into steps to improve their financial situation. There are choices each of us can make to increase our ability to generate income. Improve your education, ask for a raise, create a side business.

- Investing – When you’re heading towards financial independence, you need your money to work for you. While we don’t focus on specific strategies (most here would aim for passive index fund investing), we’re interested in long term sustainable investment returns. Money in a savings account won’t grow at the necessary rate.

I am XX years old and want to be financially independent, where do I start?

The basic tenet of FI is to spend less than you earn and invest the difference into things that earn money for you.

Spend Less/Save More

- Minimize taxes to the full extent of the law. Look into 401k/403b/457/IRA/HSA accounts as some examples.

- Reduce your living expenses. Smaller homes, apartments, rent a room. Avoid lifestyle creep as your income (hopefully) rises over time.

- Reduce transportation costs. Live close to work if possible. Avoid expensive cars – Consider bicycles, used cars, public transportation, etc.

- Learn self-sufficiency skills. Beyond the personal satisfaction in achieving something, you’ll save money. Consider cooking, mending clothes, home/automobile/bike repair, woodworking, gardening, etc.

Earn More

- If you’re in school (whether that’s high school, trade school, or college/university), focus on that first. It’s easier to be FI on $50k+/yr than minimum wage. Look carefully at your career path. Is this degree going to pay you back appropriately in the future?

- If you have a job, work more/harder/better/smarter. If you have the time, consider working extra hours and/or accepting challenging and long-distance assignments (family commitments permitting).

- Negotiate to get paid what you’re worth (see point 2 above)

Be careful about long term decisions

“Future you” may be interested in FI. Part of FI is the flexibility of having choices in the future. Be careful about locking yourself down.

- If you’re not positive you want to live in an area, avoid buying a house. Consider renting. Significantly easier to change your mind later.

- Many marriages end in divorce. Divorce is expensive. Do what you can to avoid this.

- Consider what careers are flexible and which aren’t. Nursing is known as a great career choice for people who move around (there is a need for local nurses in almost every major city in the world). Software engineering can often be done remotely. Other career choices may have less flexibility in location / availability (e.g. stock broker).

- Any loan means you are borrowing from “future you”. Be very careful about making your future self pay back a lot of money. Loans for depreciating assets (cars, electronics, etc) in particular are generally bad ideas.

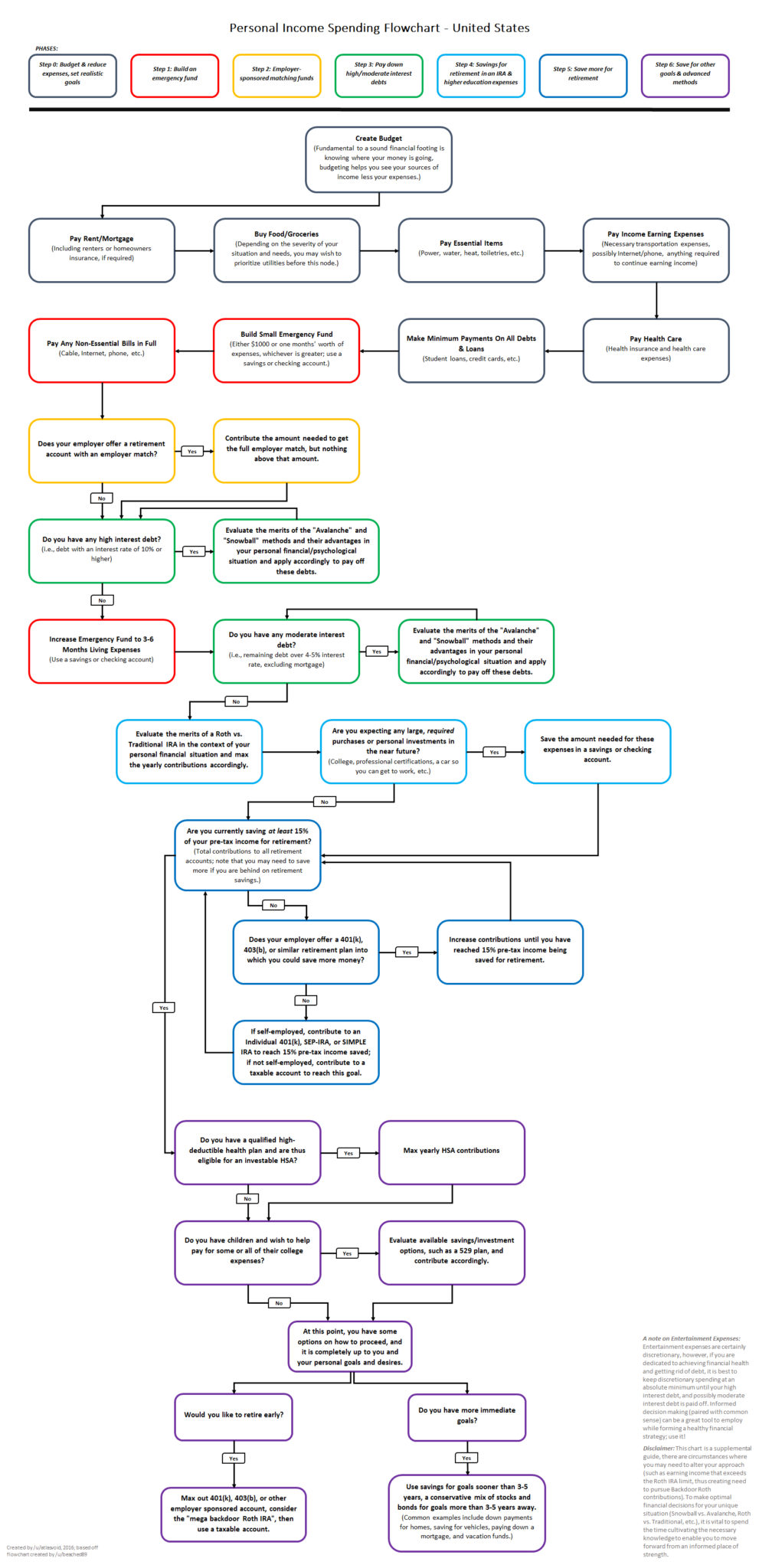

Graphical Flow Chart of Personal Finance

Step 0: Budget and reduce expenses, set realistic goals

Fundamental to a sound financial footing is knowing where your money is going. Budgeting helps you see your sources of income less your expenses. You should minimize your expenses to the extent practical – housing costs, utilities, and basic sustenance are harder to eliminate than “entertainment,” eating out, or clothing expenses.

Free online tools (like Mint.com and Personal Capital) can help you track your expenses.

Once your budget is figured out, you need to figure out what your goals are. Secure retirement? Buy a house? Save for a car? We’ll get to specifics on how to save for these a little later on.

Step 1: Build an emergency fund

An emergency fund should be a relatively liquid sum of money that you don’t touch unless something unexpected comes up. If you need to draw from your emergency fund at any time, your first priority as soon as you get back on your feet should be to replenish it. Treat your emergency fund right and it will return the favor.

How should I size my emergency fund?

For most people, 3 to 6 months of expenses is good. A larger emergency fund (e.g., 9 to 12 months) may be warranted if your income is variable or uncertain.

What if I have credit card debt?

Credit cards generally have very high interest rates (typically 15-25% APR) and that is a pretty big deal. If this applies to you, you should prioritize paying down the debt first.

A smaller emergency fund of $1,000 (or 1 month of expenses) is temporarily acceptable while paying off credit card debt or other debts with interest rates above 10%. Read Figuring the Size of Your Emergency Fund for more information.

What kind of account should I hold my emergency fund in?

Generally emergency funds should be held in safe investments you can liquidate in a hurry. FDIC-insured savings or checking accounts are the most common choice. CDs and I-bonds can be used too. Things that should not be used include stocks, credit cards, HELOCs, or anything that is volatile in value or that can be taken away without warning (such as lines of credit). Read the wiki section on emergency funds for more.

Step 2: Employer-sponsored matching funds

Once your emergency fund is set, the next step is to ensure you are contributing enough to your employer-sponsored retirement plan (if available) to get any matching funds from your employer (if they offer them). The reason you do this before paying off high interest debt is that employer matching funds are risk-free, guaranteed returns on your investments at (usually) a higher rate than your debts. This step applies to any employer-sponsored account where the employer contributes money or matches contributions (in addition to some 401(k) plans, this step applies to all SIMPLE IRAs, some 403(b) plans, some 457 plans).

For example, if your employer offers 50% matching on the first 6% of your contributions to a 401(k), you want to make sure you contribute 6% of your salary to take full advantage of the match. Instant 50% return on investment is pretty good! Be aware that 401(k) contributions must come from payroll deductions, so if you have a sum of money and want to take advantage of the match you need to increase your contribution percentage from your paycheck and use your lump sum for expenses.

What if my employer doesn’t match, or I don’t have an employer-sponsored plan?

Skip step 2, move to step 3.

What if my employer contributes to an account on my behalf regardless of whether I contribute or not?

You are very fortunate. Open the account, make sure you are getting the match, and move to step 3.

What if I am self-employed?

If you are self-employed, you can also make your own employer contributions to your 401(k) or SIMPLE IRA, but you should do this as part of step 5.

Step 3: Pay down high interest debts

After you ensure you’re taking advantage of your employer match, you should use your extra money to pay down your high interest debt (e.g., debts much over 4% interest rate).

In all cases, you should make the minimum payments on all of your debts before paying down specific debts more quickly.

There are two main methods of paying down debt:

- In the avalanche method, debts are paid down in order of interest rate, starting with the debt that carries the highest interest rate. This is the financially optimal method of paying down debt, and you will pay less money overall compared to the snowball method.

- The snowball method, popularized by Dave Ramsey, debts are paid down in order of balance size, starting with the smallest. Paying off small debts first may give you a psychological boost and improve one’s cash flow situation, as paid off debts free up minimum payments. The downside is that larger loans (that may be at higher interest rates) are left untouched for longer, costing more in the long run.

As an example, Debtor Dan has the following situation:

- Loan A: $1,100 with a minimum payment of $100/month, 5% interest

- Loan B: $3,300 with a minimum payment of $300/month, 10% interest

- Sudden windfall: $2,000

Dan needs to first pay $100 + $300 = $400 to make the minimum payments on loans A and B so the payments are recorded as “on time.” The extra $1,600 can either go towards Loan A (smallest balance, snowball method), eliminating it with $600 left to go towards Loan B, or Loan B entirely (highest interest rate, avalanche method).

What’s the best method? We tend to favor the avalanche method, but do not underestimate the psychological side of debt payments. If you think that the psychological boost from paying off a smaller debt sooner will help you stay the course, do it! You can always switch things up later. The important thing is to start paying your debts as soon as you can, and to keep paying them until they’re gone. You can use unbury.us to help you get an idea of how long each method will take, and how much interest you’ll be paying overall.

Should I be in a hurry to pay off lower interest loans? What rate is “low” enough to where I should just pay the minimum?

Depending on your attitude towards debt, you may want to stop paying more than the minimum payment on loans with low interest rates once you have paid all other loans above that threshold. A common argument is that the long-term return from investments in the stock market will likely exceed the interest rate from a low-interest loan. While this has been true in the past, keep in mind that paying down a loan is a guaranteed return at the loan’s interest rate. Stock performance is anything but guaranteed. The rough consensus is that loans above 4% interest should be paid off early in the debt reduction phase, while anything under that can be stretched out.

Shouldn’t I stretch out a loan to improve my credit score?

No. Loans should never be stretched out longer than they need to be, as you should not pay a cent in interest more than you have to for the sake of improving one’s credit score. Interest rate should be the sole factor in whether or not you pay extra on a loan or not.

Step 4: Contribute to an IRA

The next step is to contribute to an IRA for the current tax year. You can also contribute for the previous tax year if it’s between January 1st and April 15th. Try to save up to 15% of your gross income until reaching the annual limit of $6,000.

Why contribute to an IRA if I have a 401(k)?

IRAs generally have better fund choices than employer-sponsored plans because you can open one with the provider of your choice. Low cost providers like Vanguard, Fidelity, and Schwab all offer low expense ratio index funds. However, you may swap step 5 with step 4 if either of the following statements is true:

- Your employer offers an excellent 401(k), 403(b), 457, SEP-IRA, or SIMPLE IRA that has low expense index funds (i.e., a domestic stock index fund under 0.1% expense ratio, an international stock index fund under 0.2% expense ratio, and a bond index fund under 0.1% expense ratio).

- You have access to the U.S. Federal government’s Thrift Savings Plan.

One common situation where it may be advantageous to swap step 5 with step 4 is if you exceed the IRA income limit for making a fully deductible Traditional IRA contribution.

Higher education expenses

If you will be going to college in the next few years (or if you are already in college) and you will will be responsible for some college expenses (i.e., parents, scholarships, grants, etc. are not covering everything) then saving for college should take precedence over saving for retirement. College savings should be placed in low risk, low volatility investments like your emergency fund.

Consider whether the cost of any degree that you may pursue will help propel you into a career that is both financially and non-financially rewarding to you.

Note that saving for the future education expenses of children is step 6, below. Both you and your children can borrow for college, but you cannot borrow for retirement.

Step 5: Save more for retirement

After you’ve funded an IRA, if you still have money you want to put away for retirement then you should go back and round out your contributions to your employer-sponsored account (if available) so you are contributing as much as your budget allows. As in step 2, you can’t make direct contributions to your 401(k) (they have to come from payroll deductions). Adjust your contributions from your paycheck accordingly.

If you are self-employed, look into opening an Individual 401(k), a SEP-IRA, or a SIMPLE IRA for this step.

If you are not self-employed and your employer does not sponsor a retirement account, you will need to use a taxable account for this step. Ask your employer to consider providing a 401(k) or at least a SIMPLE IRA.

Before saving for other goals, you should save at least 15% and up to 20% of your gross income for retirement. If you are behind on retirement savings, you should try to save more than 15% if you can. If you can’t save 15%, start with 10% or any other amount until you are able to save more.

My 401(k) plan is awful. Should I still contribute to it?

Yes. You should always take advantage of your tax-advantaged retirement accounts before saving for retirement in a taxable account. The effect of high expenses really only starts to bite after long periods of time and 401(k) plans are quite portable. After leaving a job, you can do a rollover of your employer plan into an IRA and sometimes you can roll it into a new 401(k) with a new employer. Bad 401(k) plans can be turned into great IRAs eventually.

Step 6: Save for other goals

Once you’re on track for retirement, there is more flexibility for discretionary income. The basic options are:

- Use tax-advantaged savings for anticipated future medical and education costs.

- If you have an eligible high-deductible health plan (HDHP) and qualify, a health savings account (HSA) is a great way to save for future medical costs.

- If you wish to save for college for your kids, yourself, or other relatives, consider a 529 fund in your state.

- Save for more immediate goals. Common examples include saving for down payments for homes, saving for vehicles, paying down low interest loans ahead of schedule, and vacation funds.

- Save more so you can potentially retire early (also see “advanced methods”, below), only using taxable accounts after maxing out tax-advantaged options.

- Make an impact through giving. One of the rewards of practicing a sound financial lifestyle is that giving becomes easier. If you’re on top of your health care costs, future education costs, and you’ve made it to this step, you can help make a difference for others by giving. If you can’t afford to make monetary donations, there are other ways to give.

How you order those options is up to you, but the flowchart recommends prioritizing an HSA if you have a qualified HDHP and then a 529 if applicable to your situation.

The time frame for these goals will dictate what kind of account you save in. For short-term goals (under 3-5 years), you’ll want to use an FDIC-insured savings account, CDs, or I Bonds. If your time horizon is longer or you can afford to adjust your plans, you might consider something riskier like a balanced index fund or a three-fund portfolio (both are a mix of stocks and bonds). The best savings or investment vehicle will vary depending on time frame and risk tolerance. Feel free to start a thread with the details of your situation and we will help you.

Keep in mind that (especially for a young person) the more time your money has to grow, the more powerful the effects of compounding will be on your savings. If the goal is early retirement (even before the age of 59½), you should definitely maximize the use of any available tax-advantaged accounts (IRA, 401(k) plans, HSA accounts, etc.) before using a taxable account because there are ways to get money out of tax-advantaged accounts before 59½ without penalty.

If you are using a taxable account for any goal, you’ll want to have a decent grasp on asset allocation in multiple accounts and tax-efficient fund placement.

Advanced methods

If you’re over the income limits for a Roth IRA, pursue a backdoor Roth IRA so you can do step 4.

If your 401(k) or 403(b) plan allows after-tax contributions (this is different than making Roth contributions), consider doing the “mega backdoor Roth”.

An HSA can also be used for retirement savings.

E-Source Financial – Member Benefits

Sign Up to E-Source Financial – There has never been a better time to take your banking and finances online

62% of Americans said that they do most of their banking online

That number continues to grow daily. Why?

Most people cite two main factors; convenience and cost.

Meaning they can do what they want faster and easier for less money.

An E-Source Financial Membership helps you navigate the best options and resources for managing your finances.

Membership is for life and there are no fees.

It can be difficult selecting from the complex number of options, products, offers and tools for your banking and financial needs and services.

Let alone picking the best one for you.

E-Source helps you with our research. Have a look at the free resources we provide our visitors. Members have access to more in depth reports, recommendations and first access to new tools.

If you agree, that the time to take control of your finances is now, then sign up for your free account today and get the most with your money